Bad Credit Mortgage Loans - The Definitive Guide

Read our most important home buying updates for 2024:

Are mortgage loans available for people with bad credit? What kind of credit score does it take to get approved for a home loan? What can I do to improve my score before buying a home? These are some of the questions we will answer in this, the definitive guide to bad credit mortgage loans.

In short: Here's the nutshell version in case you're in a hurry. You will probably need a FICO credit score of 640 or higher to qualify for a home loan in the current market. If your score falls below that range, the FHA program might be your only option. There are plenty of things you can do to improve your credit situation. These numbers are not written in stone.

What is a Bad Credit Score in 2014?

The terminology can be confusing. I've often seen it written that a credit score of 720 or higher is considered "good," while a score below 620 is considered "bad." But what about the people who fall in between these two ranges? Are they better than bad? Are they less than good? In truth, the words don't really matter much. It's the numbers that count. And when you bring mortgage loans into the mix, it's a little easier to understand.

Definition: For the purposes of this article, a bad credit score is one that prevents you from qualifying for a mortgage loan. Here's how the numbers stack up:

|

FICO Score |

Category |

Description |

|

740 or higher |

Mortgage lenders will likely offer you their best interest rates, though they may require you to pay points. |

|

|

685 - 739 |

Above Average |

You could still qualify for a decent interest rate, but not the best. You might pay half a percentage more than the top-tier borrower above. |

|

640 - 684 |

You should still be able to qualify for a mortgage, but you'll pay an even higher rate than the two tiers above -- possibly a full percent higher, or more. |

|

|

639 or below |

Bad / Subprime |

You might have trouble getting approved for a mortgage loan. If you do get approved, you'll pay a much higher rate than someone with good credit -- possibly three percent higher, or more. |

Please note that these numbers represent general trends. So don't take this as the final word. I created this table by using information published from a variety of sources -- banks, credit unions, lending networks, etc. The numbers varied from one source to the next. Only a mortgage lender can tell you whether or not you meet their particular guidelines.

The purpose of this chart is to show that (A) you'll have a better chance of loan approval with a higher score, and (B) you'll pay more interest with a lower score. Is it possible to get approved for a mortgage loan with bad credit? Yes, it's possible. But the further you are down the scale, the less chance you have of getting approved.

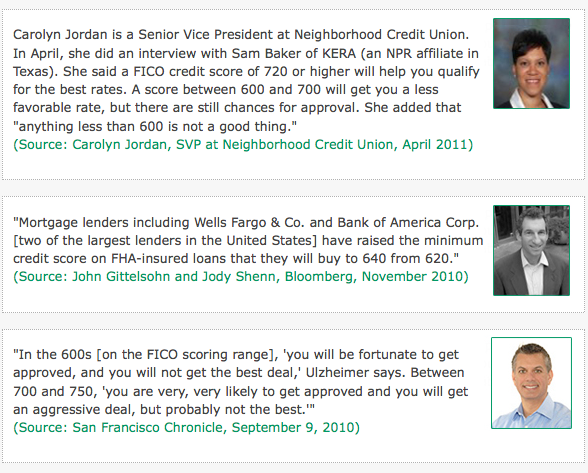

Here's what other have had to say about the credit score needed to buy a home:

Changes in Lending Standards, 2008 - 2014

You should also be aware that lending standards have changed in recent years. If I were publishing this article back in 2005, I might have started the "good credit" category at 620 on the FICO scale. But lenders have shifted their requirements upward since the housing crash of 2008. This tightening trend applies to other lending criteria as well, such as debt ratios and down payments. The bottom line: It's much harder to get a mortgage today than it was during the housing boom.

At the height of the housing boom, there were plenty of bad credit mortgage loans available. Some lenders even specialized in offering subprime loans to borrowers with low FICO scores. And then the housing crash came along. Many of them have since gone out of business (Ameriquest is a good example).

Up until 2008, credit scores didn't really matter much in the mortgage-approval process. If you had sufficient income, you could've qualified for a loan without much trouble. You simply needed to be approved by the Automated Underwriting System (AUS).

But this changed dramatically between 2008 and 2014. Automated underwriting systems are still very much in use today. In fact, manual underwriting has all but disappeared. The difference is that lenders today are paying more attention to your credit score, in addition to all of the other qualifying factors. The modern version of the AUS will automatically evaluate your credit score, your debt-to-income ratio, and the funds you have for closing. Today, your FICO score alone can make or break your chances of getting approved. It's that important.

This is why it's harder for people with bad credit to get a mortgage approval these days. That three-digit number carries a lot more weight than it did in the past.

Now that we're all caught up to the current lending guidelines, let's take a closer look at how lenders use your credit score.

How Lenders Use Your Score

Credit scores are one of several things a lender will consider when you apply for a loan. They also look at your income, the amount of debt you currently have, and the amount of money you have in the bank (i.e., cash reserves). These factors will determine whether or not you can qualify for a mortgage loan.

Why is this three-digit number so important to lenders? Why don't they offer mortgages to people with bad credit scores? To answer this question, we must look at where your scores come from and how they are calculated.

In a sense, you create your own credit score. You might not agree with the number. You might wish it were higher. But the number itself is a direct reflection of your previous financial activity. The image above shows how this activity is turned into a score, through a scoring system such as the FICO model or the VantageScore.

When you borrow money ... when you make payments toward a debt ... when you have problems paying your bills ... all of these things are reported to the three credit-reporting companies shown above. So this data shows up on your credit reports. But lenders don't usually look at the reports themselves -- they look at the three-digit scores that are based on those reports. But it all starts with you! It all starts with how well you repay your debts.

Here's how it relates to bad credit mortgage loans:

Your credit score is designed to show lenders how likely you are to repay your debts. In theory, a lower FICO score suggests a higher likelihood of default. (By way of terminology, someone "defaults" on a loan when they stop making their payments on time.) Obviously, this is something the lender wants to know. They want to know how likely you are to make your mortgage payments. So they look to the "predictive analysis" model created by FICO, as well as the newer VantageScore created by the reporting companies.

Of course, the credit score isn't a crystal ball. It doesn't predict how a borrower will act in the future with any certainty. It only shows how the borrower has behaved in the past. Still, it's the best tool lenders currently have for predicting risk. And that's why bad credit mortgages are hard to come by these days. A lower FICO score suggests a bigger risk for the lender -- and they're not taking many risks these days.

You'll also need a certain credit score to qualify for private mortgage insurance, or PMI. This insurance is required on all mortgages with a loan-to-value ratio higher than 80 percent. So if you put down less than 20 percent on the loan, you'll have to pay PMI. This means you have to meet two sets of credit guidelines -- the lender's as well as the PMI company's. This makes it even harder for people with poor credit to get a mortgage loan.

So what is a bad-credit borrower to do? Are there any loan options available, or just a bunch of dead-ends? Let's talk about some of the loan programs that are better suited to subprime borrowers.

FHA Mortgage Loans for People with Bad Credit

At the beginning of this article, we talked about the definition of bad credit. I defined it as a FICO score of 639 or below. If you fall into this range, you'll have fewer mortgage options than a borrower with good credit. Sorry, I don't make the rules. But this doesn't mean you're out of luck entirely. There are still some lenders willing to work with borrowers in this category. And you've got nothing to lose by trying.

You might want to look into the FHA loan program, in particular. Here's why...

FHA loans are made by "regular" lenders in the primary market, just like any other type of mortgage. The difference is that FHA loans are insured by the federal government (through the Federal Housing Administration, which is part of HUD). The insurance is designed to protect the lender's investment. If the homeowner defaults on the mortgage, the FHA will cover the lender's losses.

What does this have to do with bad credit mortgage loans? Everything. Lenders are often more flexible when approving you for an FHA loan, as compared to a conventional mortgage that's not insured by the government. This applies to their credit requirements as well.

If your FICO score is below 640, you'll have a hard time qualifying for a conventional mortgage loan. This is the minimum cutoff point for most lenders. Additionally, the mortgage insurance (PMI) company might require an even higher score than the lender. And you'll need PMI coverage if you make a down payment of less than 20 percent.

This is where the FHA program proves useful. People with bad credit can often qualify for an FHA mortgage, even when the conventional loans are not available to them. It's like having a side door to homeownership when the front door has been closed on you.

With all other things being equal, you can get approved for an FHA loan with a lower FICO score. How low? It depends on the lender you use. You'll need to apply for the program through an FHA-approved lender. So you have to meet two sets of guidelines -- the lender's and the FHA's. Here's the difference:

|

FHA Requirements |

Lender Requirements |

|

The FHA has a two-tiered system for credit scores. For basic program eligibility, they require borrowers to have a credit score of at least 500. In order to qualify for the 3.5-percent down-payment option, borrowers will need a score of 580 or above. |

FHA-approved mortgage lenders often impose their own credit guidelines, on top of those used by the FHA. These are referred to as "overlays." Some lenders require a FICO score of 640 or higher. Others will allow lower scores. |

As you can see from the table above, a person with bad credit may or may not be approved for an FHA loan. It depends on the overlays used by the lender. Still, this program is often the best option (or the only option) for a borrower seeking a bad credit mortgage.

Update: In February 2011, the New York Times reported that Wells Fargo (the largest mortgage lender in the United States) was lowering its minimum score to 500 for some FHA loans. This means their bottom-end cutoff would match the one used by the Federal Housing Administration. It also means that more people with bad credit could qualify for financing through Wells Fargo. That was the case when this was article was published, in May 2011. You would have to speak to a Wells Fargo representative to see if it still applies.

How to Improve Your Score Before Buying a Home

Improving your FICO credit score will make things much easier for you. It could save a lot of money as well. A higher score will help you get approved for a loan, and it will also help you secure a better interest rate. When you spread that lower rate over the many months of the payback period, you could end up saving thousands of dollars.