U.S. Real Estate News Delivered Weekly

Subscribe to our newsletter to receive independent U.S. housing market news and updates, straight to your inbox every Thursday at 10:00 a.m. (CST).

For over 20 years, we've tracked the trends that shape the U.S. residential real estate scene. We now distribute those insights in an easy-to-digest weekly newsletter.

Subscribe to Housing Weekly today to keep up with an ever-shifting market.

Two Decades of Real Estate Market News

A lot of U.S. real estate news is written to trigger panic or hype. Clickbait headlines focus on extreme predictions, rather than underlying economic realities.

We take a more grounded approach.

For more than 20 years, the Home Buying Institute has monitored, analyzed, and reported on housing market conditions across the U.S.

We've kept our readers informed through major economic cycles, booms and busts, and ever-changing supply and demand conditions.

Why Our Readers Trust Us

- Expertise: Led by market analyst Brandon Cornett, we've been closely monitoring the U.S. housing market for more than two decades.

- Independence: We aren't real estate brokers or lenders. This independence allows us to deliver real estate news that's free from conflicting interests.

- Convenience: We track a variety of housing market and economic indicators, so you don't have to sift through the data yourself.

In short: If you want to receive useful and informative real estate reporting every week, with a veteran analyst as your guide, this newsletter is for you.

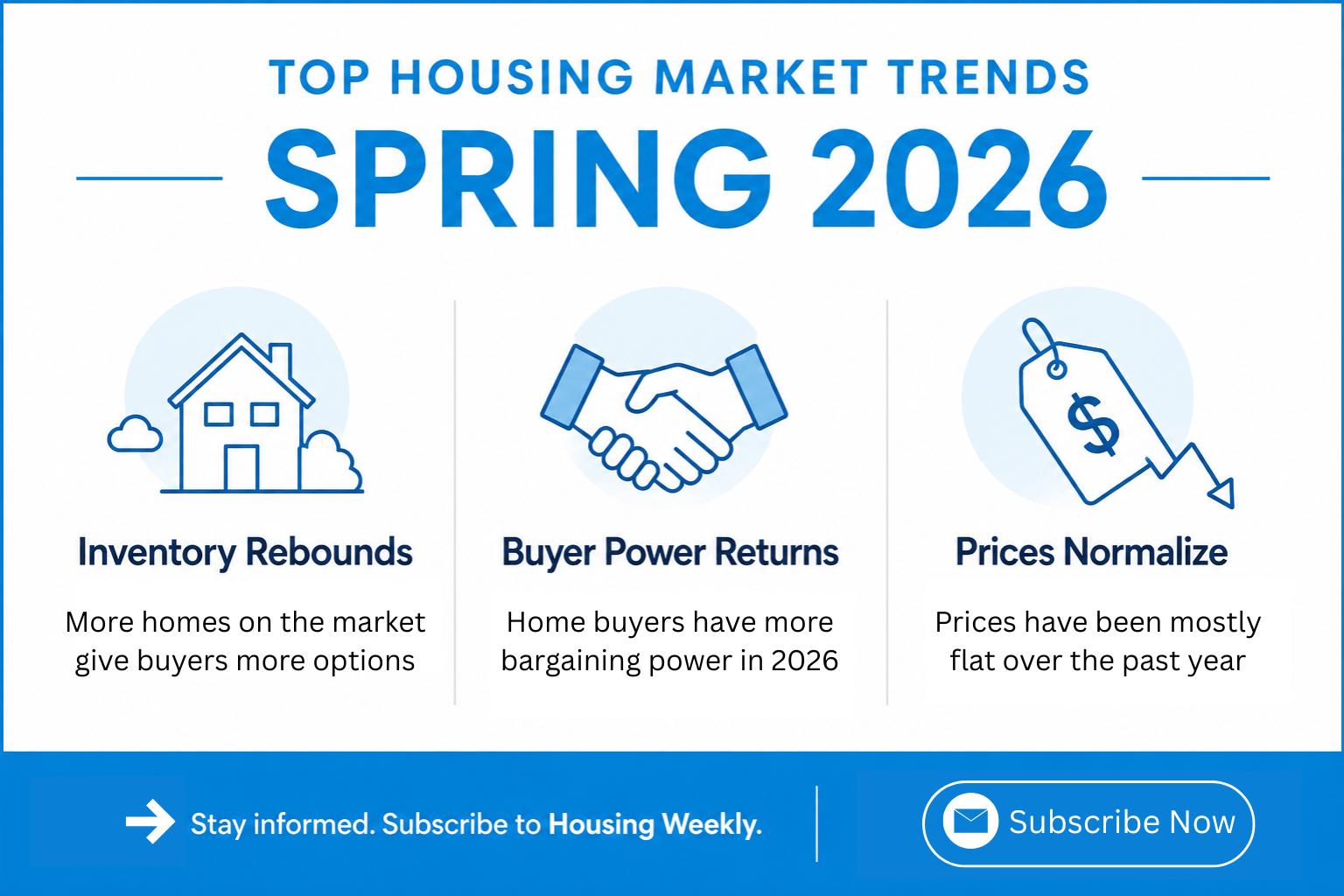

Housing Market Update: Spring 2026

Our newsletter delivers a steady stream of real estate news to help you keep up with important market trends, including home prices, sales activity, market "temperature" and more.

Here are some of the biggest stories we're tracking in spring 2026.

1. Home prices are flat across the country.

The days of rapidly rising home prices are over for now. According to recent data from Zillow, the average U.S. home value went up by only 0.6% over the past year. While prices are still ticking up slightly in a few specific cities, the general trend across the United States is a very stable, flat pricing environment.

2. Higher mortgage rates are limiting buyer demand.

Interest rates are the main reason the real estate market has slowed down. With the average 30-year fixed mortgage rate hovering in the mid-6% range this spring, many potential buyers simply cannot afford to buy a home right now. This drop in purchasing power is keeping the overall number of buyers low.

3. Buyers are gaining more negotiating power.

Sellers no longer hold all the cards like they did a few years ago. Because there are more homes available for sale now and properties are sitting on the market longer, buyers finally have the room to negotiate. Bidding wars have become rare in most neighborhoods.

Samples: Previous Real Estate Market Updates

The best way to get a feel for the real estate news we publish is to read a few issues. Here are three recent newsletters that offer U.S. housing market updates and analysis:

More Sellers Are Taking a Timeout in 2026

The latest data from Redfin reveals a rising wave of home delistings nationwide, signaling that more sellers are taking a "timeout" as price-sensitive buyers refuse to overpay.

Renting Cheaper Than Buying in Most Cities

A new report confirms what most people across the United States already know: renting a home is usually cheaper than buying one. On average, renters in the U.S. spend about $920 less per month than homeowners.

Will the Housing Market Stall This Spring?

The spring housing market started 2026 with real momentum, but rising mortgage rates and economic uncertainty have created new headwinds.

Questions?

If you have questions about the Housing Weekly newsletter, or the U.S. real estate news it delivers, please email editor@homebuyinginstitute.com.