The Homeowner's Guide to Mortgage Refinancing Quotes

Read our most important home buying updates for 2024:

If you've been researching the mortgage refinance process for any length of time, you've probably seen a lot of offers for "free quotes." They leap out at you from newspaper ads and website banners. They talk about huge savings and low interest rates. They are riddled with disclaimers and fine print. But what is a mortgage refinancing quote, exactly? How does the quoting process work? Let's take a closer look.

This website is a learning center for homeowners. But it's also an action center. You can research every aspect of the refinancing process from right here on our website. If you're ready to move forward with the process, you can use the link provided above.

Mortgage Refinancing Defined

We will talk more about refinancing quotes later. First, I want to make sure you understand what it means to refinance your home loan. What you're doing is replacing your existing mortgage with a new one. You're paying off your current debt obligation by taking on a new loan.

It's actually very similar to the process you went through when you first bought the home. The loan application, the paperwork, the credit check -- you'll go through all of that again when you refinance your mortgage.

Why would someone do this? What's the point of replacing one loan with another? People use refinancing to achieve different goals. The most popular reasons are:

- To get a lower interest rate (and a lower payment)

- To switch from an adjustable to a fixed-rate loan

- To pull cash out of the house by leveraging equity

- To shorten the length of the loan's term

You could even accomplish a couple of these goals at the same time. Because you're reading this article right now, you can probably identify with one or more of the goals listed above. It's what brought you here. Now you're probably wondering two things: (1) What does it take to refinance my home, and (2) how do I get mortgage refinancing quotes from lenders? Let's start with the first question. And remember, you can get quotes at any time by using the link at the top of this page.

Basic Requirements for a Refi Loan

Many homeowners think they are entitled to a refinance loan simply because they own a home. Nothing could be further from the truth. Each year, thousands of homeowners get turned down for refinancing. There are many reasons for this.

Here are the three most common reasons for denial:

- The homeowner does not have enough equity in the home.

- The homeowner's credit score is too low for mortgage approval.

- The homeowner has too much debt to qualify for the new loan.

You should already know where you stand in each of these areas. If you don't, you've got some homework to do. You should not request a refinancing quote until you know how you measure up in these areas. Check your credit score. Get an estimate of your home's current market value, and use that to measure your equity. Figure out what your debt-to-income ratio is.

I'll explain how to perform these tasks in a moment. First, let's talk about the basic qualifications for refinancing a home loan.

1. What's your credit score?

Lenders have increased their credit-score requirements since the housing crisis first began. This applies to refinancing as well as purchase loans. You will probably need a FICO score of at least 640 to qualify for a refi loan. Some lenders may require an even higher score. But this is certainly not written in stone. If you have a lot of equity in the home, the lender might be more flexible with their credit requirements.

Lenders will check your score shortly after you apply for a mortgage refinancing quote. But you should find out where you stand now, by checking your own score (here's why).

2. How much equity do you have?

Equity is the amount of ownership you have in your home. To determine this number (expressed as a percentage), you would subtract your current mortgage balance from your home's market value. If my home is worth $300,000, and I currently owe $150,000 on my loan, then I have 50 percent equity in the house.

When you apply for a refinancing quote from a lender, they will eventually send a professional appraiser to your home. The appraisal is usually one of the first steps in the process, because it could make or break the deal. Think about it from the lender's perspective. They don't want to tie up one of their underwriters until they figure out what your home is worth -- and whether or not the deal can go forward.

If your property values have gone down since you first bought the home (a common trend after the housing crash), you might not be able to refinance at all. If home prices are still going down in your area, I can almost guarantee you won't qualify for a refi.

How much equity do you need to refinance? This will depend on the lender. There's no magic number that applies to all scenarios. But most lenders want to see that you have at least 5 percent equity in the home. Others will require 10 percent. If you want to do a cash-out refinance, you'll probably need at least 10 percent equity.

When you gather mortgage refinancing quotes from lenders, ask about their equity requirements. They probably have an info sheet they can send you with their basic requirements. They might even have it posted on their website, or on their application forms.

Does It Make Sense to Refinance?

Does it make sense for you to refinance right now? Will you be able to accomplish your goals during the process? Will your savings be greater than your closing costs? These are the questions you need to ask before moving forward.

Mortgage refinancing quotes can actually help you answer some of these questions. For example, let's assume your primary goal is to secure a lower interest rate on the loan. But in reality, that's only half of your objective. It's not enough to lower your payment. You need to save enough money over the term of the new loan to justify paying your closing costs. Your savings must exceed your closing costs in order for the loan to make sense -- unless you're just trying to tap your equity.

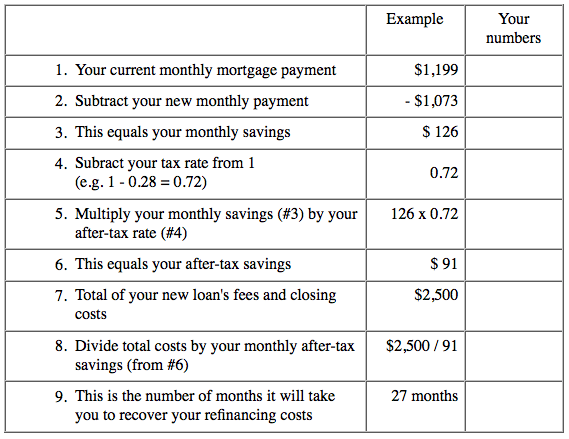

This worksheet from the Federal Reserve shows how to calculate your "break-even point" or BEP. You should familiarize yourself with this term, and what it means.

Some lenders will help you determine your break-even point at the time you obtain a refinancing quote, or shortly after that. Others will leave the math up to you.

Getting Free Quotes from Lenders

So you've checked your credit score, you've gathered your financial documents, and you feel you're in a pretty good position with your equity. What next? How do you start gathering quotes from lenders? There are several ways to go about it:

- You have a mortgage loan right now. So you already have an existing relationship with a lender. In some cases, you can get the best rates from the lender you're already working with. This is especially true if you've been making all of your payments on time. The process might be a little more streamlined, as well. Just make sure you get an offer from at least one other source, for the sake of comparison.

- You could also use an online network of lenders to get mortgage refinancing quotes. This can be a real time-saver, because it allows you to gather information from several companies at once.

- You could work with a mortgage broker. The benefit here is that the broker can match you with the best lender, based on your qualifications and refinancing goals. Just find out who pays the broker's fee. Sometimes the lender will pay the fee. Other times, they'll pass the cost along to the borrower (in the form of closing costs).

How you get quotes is not really that important. The most important thing is to get at least two offers so you can compare rates and fees. Remember, the lender's closing costs are a key part of the puzzle when determining your break-even point. So it pays to shop around.